Posts Tagged ‘borrowing’

An introduction to credit scoring

A credit score is a three-digit number that can determine whether a loan application is accepted. Borrowers with lower credit scores are often charged higher rates of interest. Of course, we don’t do that at Central Liverpool Credit Union. We prefer to see our members as human beings, not numbers. We obtain credit scores, but…

Read MoreWe are simplifying our loans

Later this week – and before launching online loan applications – we are simplifying our loan products. Member loans We want to reward savers with a reduced rate of interest. If you’ve been a member of the Credit Union for more than two years AND have more than £500 in savings you can apply for…

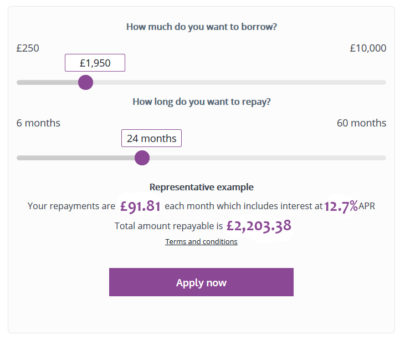

Read MoreApplying for loans online

From April you will be able to apply for a loan online. We will always welcome people into our offices. But from April you will be able to apply at a time and place of your choosing, including from your mobile without the need to download an app. We’ve made this process as simple as…

Read MoreChristmas loans

Christmas loans from Central Liverpool Credit Union: There’s only 11 weekends until Christmas! The cut-off date for Christmas loans is 26th October. If accepted a loan received by this date is guaranteed to be paid in time for Christmas. We will still look at loans for Christmas until 20th December. However there is no guarantee…

Read More